The Emperor Has No Algorithms: The Bridgewater Bubble Bursts

For over two decades, Bridgewater Associates founder Ray Dalio boasted that his $168 billion hedge fund had found the "holy grail" of investing.

But like many of Wall Street's "Masters of the Universe," Dalio turned out to be just another bullshitter.

At least, that's what Rob Copeland argues in his new book, The Fund: Ray Dalio, Bridgewater Associates, and the Unraveling of a Wall Street Legend.

Poor Boy From Long Island Makes Good

At his peak, Dalio cut a remarkably confident figure.

Dalio lectured foreign policy experts on his worldview. He imparted his wisdom through his widely promoted "Principles." He touted Bridgewater as a hyper-transparent money machine driven by the Darwinian revolutionary logic of the "survival of the fittest.”.

Dalio often touted his modest beginnings and his improbable road from Long Island to Harvard Business School.

He was far more reticent about having married into the Vanderbilt fortune- a leg up on life he exploited with alacrity.

Take it from a poor boy from Pittsburgh who also made it to Harvard…

There’s nothing quite like the combination of “f*** you” money and an entree into New York high society to boost a young man’s career.

Signs of Sorcery

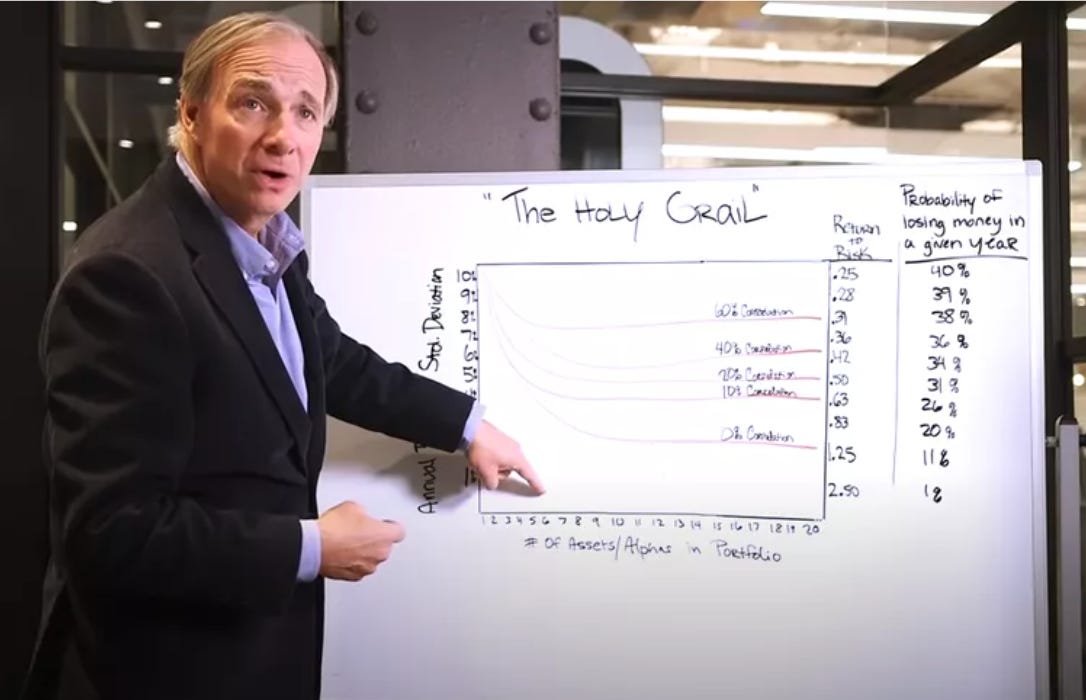

Dalio preached "radical transparency." Yet the opaque trading formulas underpinning his "investment engine" remained tightly guarded secrets.

Hindsight is always 20/20. But there was always something about Dalio that did not add up.

Rivals struggled to reconcile Bridgewater's towering reputation with mediocre returns.

On the one hand, Bridgewater's "signals" offered uncanny forecasts, generating ample alpha. After all, that's how it became the world's largest hedge fund, having navigated 2008's carnage with aplomb.

On the other hand, Bridgewater’s returns over the past decade were positively pedestrian. And Dalio got a lot of things wrong. Yet, its leading fund floated on calm waters, untroubled by Dalio's errant forecasts.

Dalio claimed adherence to cold quantitative reasoning over hot-blooded instinct.

But it turns out that the wizard behind the curtain was a blowhard and a mountebank.

Bridgewater's investing "secret "was that there was no "secret."

Like the fraudulent schemes of history's great charlatans, Dalio's investment "holy grail" was an illusion. His vaunted signals were as real as the potions of quacks and alchemists.

Dalio's pronouncements proclaimed quantitative purity.

Yet, what he imparted in books and interviews were generic platitudes.

Dalio's evasiveness soon aroused suspicions.

Newsletter writer Jim Grant scoured Bridgewater's public filings. Strange math, odd loans, winks, and nods convinced Grant to issue a critical report, stoking unease.

Bridgewater badgered Grant to recant his charges. He did. Still, the apologizing Grant remained baffled.

Smelling rot, Harry Markopolos – the analyst who tried to out Bernie Madoff-also chimed in.

To Markopolos, Bridgewater eerily echoed Madoff's steady returns amid market chaos.

Fellow skeptics and hedge fund mavens Bill Ackman, Kyle Bass, and David Einhorn concurred, fueling further scrutiny.

After all, these were also alpha dogs playing in the same sandbox as Bridgewater, but with different results.

Markopolos notified the SEC: In his view, Bridgewater equaled Ponzi.

Though Markopolos sparked inquiries, the SEC found no fraud.

The SEC's insipid conclusion?

While no Ponzi, Bridgewater was just complexity cloaking straightforward bets.

Dalio's Inner Circle

Like legendary swindlers, Dalio seduced his marks with elaborate fictions. His façade of quantitative purity shifted attention away from Bridgewaters' ever more humdrum returns.

Echoing Madoff, not even its employees knew how Bridgewater made its money. A mere dozen among 2000 employees handled trading. The rest just researched or paper-pushed.

Only an elite inner circle was allowed a glimpse behind the curtain. Dalio bought their silence with lifelong contracts and fat paychecks.

It was this cabal that purportedly turned Dalio's Principles into market profits. Their methods were too arcane for outsiders to comprehend, let alone replicate.

Publicly, Dalio touted a Darwinian investing process where the best ideas prevailed.

To this end, Dalio feigned participation in pseudo-democratic debates. With cameras rolling, minions argued economic minutiae and geopolitics.

But it was a mere pantomime of radical transparency performed for the benefit of clients. The results of these marathon sessions rarely influenced actual trades.

Upfront, Dalio, the smiling showman, theatrically wowed the investors and the media.

The mechanics of the Bridgewater's magic were hidden from view in the back.

Only by obscuring reality with artifice could Bridgewater maintain its aura of omniscience.

Dalio the Dictator

Yet, Bridgewater harbored another secret.

It had a toxic corporate culture that resembled more a North Korean-style dictatorship than a revolutionary quant shop.

Mao had his "Little Red Book." Dalio had his "Principles."

Bridgewater touted its predictive brilliance. But Bridgewater's vaunted AI was a mirage; its signals were mere props in an illusionist's show.

Dalio alone directed trades, conjuring profits through simplistic trend-chasing rules. Bridgewater's fortunes rose and fell on one man's mediocre magic. His gift was not for seeing the matrix but for mythmaking.

This worked in less sophisticated times. And Dalio's preternatural bearishness paid off in 2008.

But in time, copycats bested Dalio's dated formulas, powered by brute-force computing.

And yet…

Decades of marketing mystique maintained the myth of his investing sorcery. So, despite trailing markets, assets flooded in from credulous global clients.

But with a decade of poor returns, some members of the Inner Circle compiled Dalio's track record.

It turned out that the alpha dog's predictive brilliance was a myth. His hit rate was no better than coin flips.

The Inner Circle presented the data tremblingly to the king.

Dalio crumpled up the paper and threw it in the garbage,

For all the talk of Darwinian logic, Dalio was unwilling to brook evidence of his invincibility.

Extinguishing all doubt was vital to preserving Dalio's aura of infallibility. Like a Communist dictator, he could not countenance questioning. The façade of quantitative purity must be maintained, even as returns suffer.

The Myth Unravels

Still, chinks in the armor appeared, shrinking Bridgewater's pile.

And with it, so did Dalio's stature.

In 2008, Ben Bernanke sought Dalio's advice. His successor, Janet Yellen, failed to return his phone calls.

But Bridgewater plodded on, preserving its brand over performance.

As returns languished, Dalio leaned on his unmatched access to insider economic intelligence.

Lavishing foreign dignitaries with helicopters and hollow flattery, he extracted privileged information from around the globe. He courted central bankers and despots with choreographed charm offensives. He was ever hungry for early warnings on rate shifts, stimulus, and currency pegs.

Ultimately, his fortunes were less tied to investing vision than an unparalleled monopoly over the whispers of the influential. His returns sprang not from perpetually peerless predictions but perpetual access to power's ear.

Ultimately, Bridgewater profited more from garden variety guile than groundbreaking algorithms.

Dalio's true life's work was to subject the 1,600-odd people who worked for him to ever more baroque and dystopic psychological manipulations.

In short, the story of Bridgewater is less a story about high finance.

Instead, it is about, as the New York Times put it

"how a man of surprising mediocrity used money to control and humiliate, and how much people abased themselves for it."

Great article on Dalio. I think I will buy the book. i have read some of his stuff. He says (in too many words) what any student of history SHOULD already know.

In early middle age I began to read in earnest books on finance. They ranged from non-fiction novel style books (such as "When Genius Failed") to how to books (such as "Unconventional Success"). Some were highly interesting and entertaining, such as Niederhoffer's "Education of a Speculator." A handful were revelatory, such as Taleb's "Black Swan." One I thought was a real dud, probably because of my legal training and experience, Truell and Gurwin's "False Profits" about BCCI, Clark Clifford and Robert Altman. As I read it I kept thinking that the case against them sounded like a lot of guilt by association and would not succeed in criminal court. Despite the book's glowing reviews. And that proved to be the case. Mark Hulbert likes to tell the story about going on Rukeyser's show with Al Frank and Joe Granville, the former a good newsletter producer, the latter a poor newsletter producer. But he suspected that the latter may well have sold more newsletters from that appearance because of his energetic confidence. Something in the human psyche allows bluffers to prosper at least until the house of cards collapses, as some recent high profile disasters have illustrated.